South Florida is one of the most vertically dense residential markets in the United States.

Brickell. Sunny Isles. Edgewater. Aventura. Downtown Fort Lauderdale. Naples waterfront towers.

Thousands of high-rise units. Billions in residential asset value.

Yet most pricing workflows still operate horizontally.

ZIP code.

Building name.

Square footage.

Recent sale date.

That works in suburban markets.

It creates blind spots in vertical ones.

The Problem No One Talks About

Two units in the same tower can have:

• Identical square footage

• Same layout

• Similar interior finishes

But materially different market outcomes.

Why?

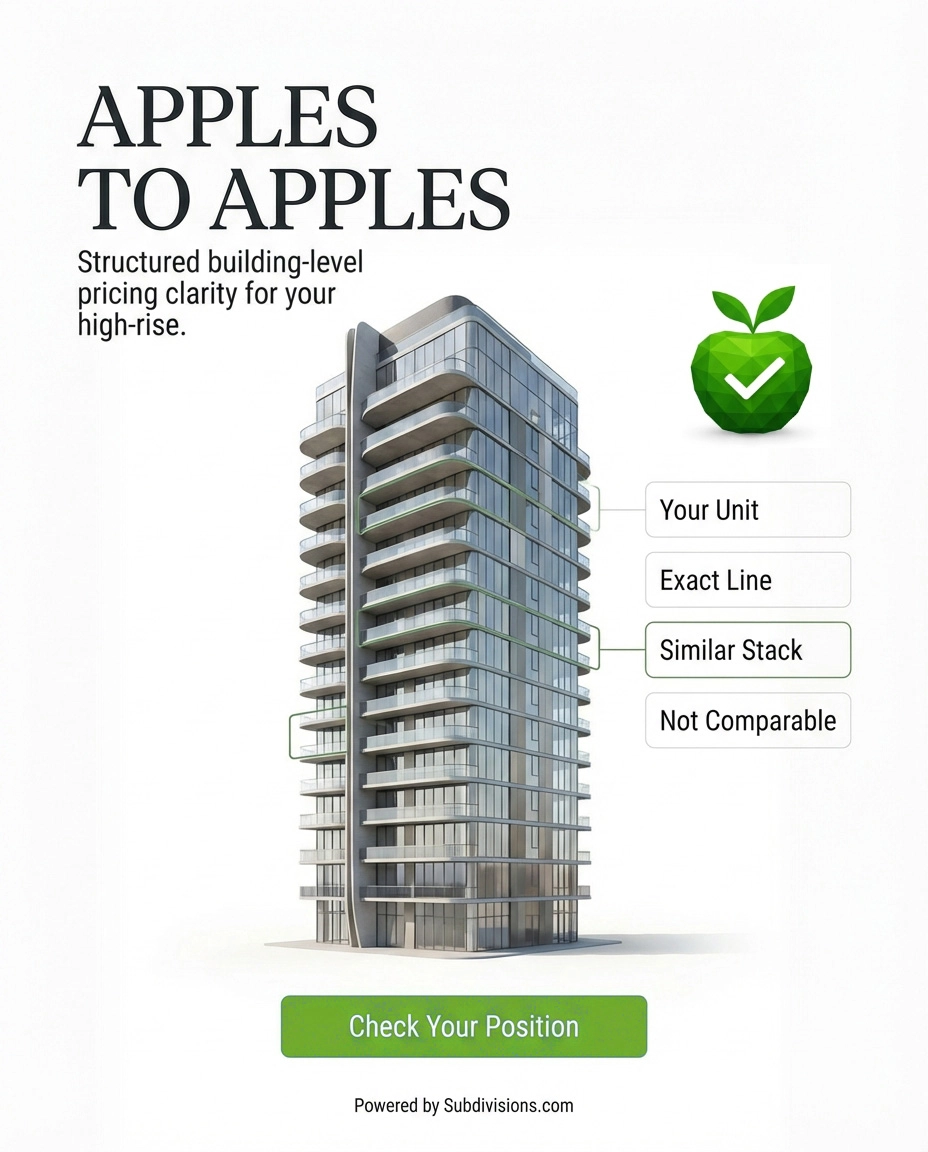

Because in high-rise environments, pricing behaves vertically.

Inside:

• Stack 04

• Stack 08

• Upper-tier floors

• Water-facing exposures

• Interior-facing exposures

And, most importantly:

Against active competition inside the same line.

When comps are aggregated across the entire building instead of isolated by stack, incremental distortion begins.

It’s rarely dramatic.

It’s incremental.

And incremental misalignment is the most expensive kind — because it hides inside “close enough.”

At Scale, “Close Enough” Becomes Expensive

In South Florida luxury towers, unit values often range from $800,000 to $5M+.

A 4% misalignment on a $2M unit equals $80,000.

Across 15 units in the same tower, that’s $1.2M in exposure.

Not necessarily lost — but tied up in:

• Extended days on market

• Carry costs

• Repricing cycles

• Absorption drag

• Capital inefficiency

In high-density vertical markets, pricing discipline is not cosmetic.

It is operational.

Why Traditional Tools Flatten Vertical Markets

Most residential data platforms were built to answer one question:

“What did something similar sell for?”

That works when “similar” means:

Same neighborhood.

Same lot size.

Same style.

But in high-rise towers, similarity must be defined structurally:

Same line.

Same exposure.

Same floor tier.

Same active competition window.

Without that isolation, pricing decisions rely more heavily on discretionary adjustment.

Discretion scales poorly.

The Operational Reality in South Florida

South Florida has:

• Heavy international ownership

• Seasonal sellers

• Concentrated vertical inventory

• High average unit values

• Developer-held remaining inventory

• Bulk investors with multiple units

When inventory is dense and capital exposure is high, micro-context matters more than macro trends.

A building-level median price does not tell you how Stack 03 is performing against Stack 09.

But that difference can determine:

• Absorption velocity

• Seller confidence

• Developer release strategy

• Portfolio alignment

The Shift: From Horizontal Aggregation to Vertical Structure

Enterprise micro-market intelligence is not about predicting value.

It’s about structuring context.

Instead of aggregating by building, structured intelligence isolates:

• Line-by-line pricing behavior

• Floor-tier distribution

• Active vs. sold alignment within identical stacks

• Intra-building competition density

This reduces comp-selection noise.

It increases internal defensibility.

It shortens pricing debate cycles.

It improves capital alignment.

Who Benefits Most in South Florida?

Developers With Remaining Inventory

Structured stack-level visibility reduces internal pricing drift and improves release discipline.

Institutional Condo Holders

Standardized micro-market context across multiple units reduces portfolio variance.

Asset Managers

Improved absorption clarity inside dense towers enhances exit modeling.

BPO & Valuation Oversight Firms

Faster stack-aware comp review improves consistency and reduces revision cycles.

Lenders With Condo Exposure

Improved collateral sensitivity review in vertical markets.

This is not a consumer marketing tool.

It is infrastructure for dense residential capital environments.

Subdivisions.com: Built for Vertical Markets

Subdivisions.com structures residential market data at the subdivision and building level.

In high-rise environments, it organizes information vertically:

• Stack-aware comparisons

• Floor-based clustering

• Active vs. sold normalization

• Pricing distribution inside the building

It does not replace appraisal methodology.

It does not issue valuation opinions.

It structures context where pricing actually competes.

Inside the building.

Why This Matters Now

South Florida’s condo market is capital-intensive, globally exposed, and highly competitive.

In dense vertical environments, pricing mistakes rarely explode.

They accumulate.

The future of residential asset intelligence — particularly in high-rise markets — is not broader.

It’s deeper.

And in South Florida, pricing risk isn’t in the ZIP code.

It’s in the stack.

Comments