For decades, the homebuying process followed a familiar pattern.

A buyer would search for homes on one platform, connect with a real estate agent through a brokerage, and secure financing through a completely separate lender. Each step of the transaction lived in its own ecosystem, loosely connected but largely independent.

That model is now changing — quickly.

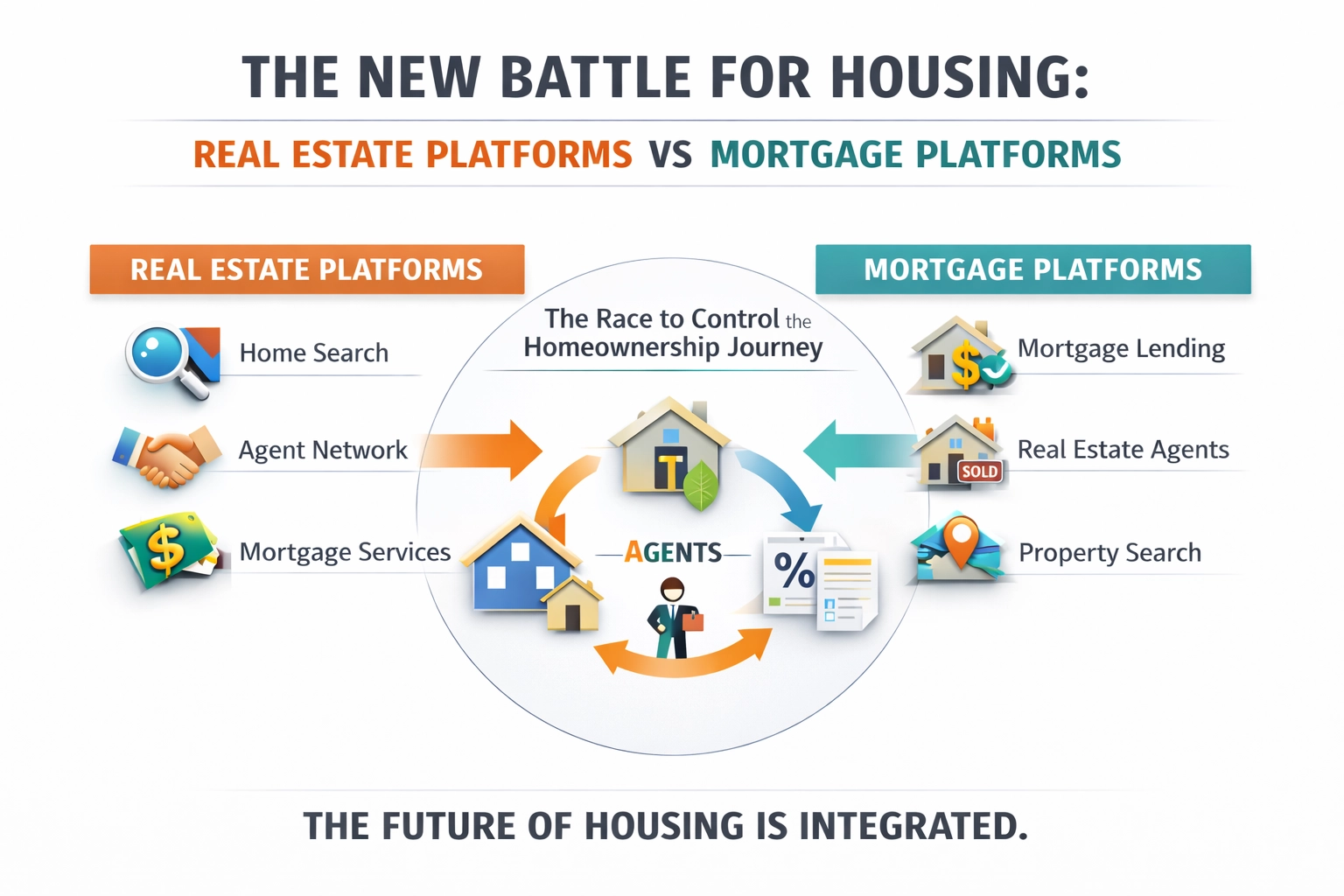

A new competitive landscape is emerging across the housing industry, where real estate platforms and mortgage companies are racing to control more of the homeownership journey.

Zillow’s expansion into lending

Zillow is no longer just a home search platform.

In 2018, Zillow entered the mortgage business by acquiring Mortgage Lenders of America, which was later rebranded as Zillow Home Loans. The company now offers prequalification, mortgage applications, and lending services directly to buyers browsing homes on its platform.

The strategy is clear: if the home search begins on Zillow, the company wants to remain part of the process all the way through financing.

By integrating search, agents, and mortgage services, Zillow aims to keep the consumer within its ecosystem from the first property search to the closing table.

Rocket moves in the opposite direction

While Zillow expanded into mortgages, Rocket Companies has been moving toward real estate.

Rocket, already one of the largest mortgage lenders in the United States, recently announced plans to acquire Redfin, the well-known home search platform and brokerage. If completed, the deal would combine Redfin’s real estate search and brokerage network with Rocket’s lending infrastructure.

The goal mirrors Zillow’s strategy — but from the opposite direction.

Rocket wants to connect home search, real estate agents, and mortgage financing into a single integrated platform designed to guide consumers through the entire homeownership process.

The race to control the homeownership pipeline

These moves reflect a broader shift in the housing industry.

Historically, the homebuying process looked like this:

Search for homes

Connect with an agent

Apply for a mortgage

Three separate steps, often handled by three different companies.

Today, major platforms are attempting to bring those steps together. The company that controls the starting point of the home search gains a powerful advantage: it can influence agent relationships, financing choices, and the broader transaction process.

In other words, the competition is no longer just about listings or mortgage rates.

It is about who owns the homeownership pipeline.

The missing layer in housing platforms

As real estate platforms and fintech companies move toward deeper integration, one structural challenge remains.

Most housing platforms still organize the market using broad geographic averages — cities, ZIP codes, or general neighborhoods.

But residential pricing rarely behaves that way.

In practice, pricing dynamics often form at a much more granular level:

subdivisions in single-family communities

individual condo buildings in urban markets

stack, tier, and exposure differences inside high-rise developments

true competitive sets among similar properties

These micro-market dynamics can significantly influence pricing, yet they are often lost within broader geographic averages.

In markets dominated by vertical living and community-based housing — such as South Florida — these distinctions become even more pronounced.

Why data structure will matter more

As the housing ecosystem becomes more integrated, the importance of accurate market structure will only grow.

Real estate platforms depend on reliable competitive comparisons.

Mortgage lenders rely on valuation clarity to support underwriting decisions.

Agents need credible pricing narratives when presenting to sellers.

Consumers, meanwhile, increasingly expect transparency and precision throughout the homebuying process.

Without a deeper understanding of how residential markets are structured, even the most advanced platforms may struggle to interpret pricing signals accurately.

The risk of falling behind

For companies still operating within the traditional fragmented model, the risks are growing.

As real estate platforms and mortgage providers consolidate and integrate their services, the gap between integrated ecosystems and independent players may widen. Companies that fail to adapt could become increasingly dependent on larger platforms that control consumer access through search, financing, or transaction infrastructure.

Over time, this shift could reduce visibility, compress margins, and weaken direct relationships with buyers and sellers.

In an industry where distribution and data are becoming strategic assets, ignoring these structural changes may leave some market participants struggling to remain competitive.

The next phase of the housing ecosystem

The convergence of real estate platforms and mortgage companies signals a fundamental change in how the housing industry operates.

The next generation of housing platforms will not simply connect listings with buyers or mortgages with borrowers.

They will aim to support the entire homeownership journey.

Search, agents, financing, and transaction services are increasingly becoming part of a single ecosystem.

The question for the industry is no longer whether these systems will converge.

The real question is whether the underlying market intelligence supporting them will evolve at the same pace.

Because in residential real estate, the platforms that truly understand how pricing forms inside the market may ultimately shape how the entire ecosystem operates.

Comments