Residential pricing models were built for neighborhoods.

High-rise assets don’t behave like neighborhoods.

They behave like vertical micro-markets.

And when that distinction is ignored, pricing risk quietly compounds.

The Structural Mistake in High-Rise Pricing

In most residential workflows, comparable selection follows a predictable pattern:

Filter by building

Filter by size

Filter by recent sale date

Adjust for floor and view

This approach is efficient.

It is also structurally imprecise.

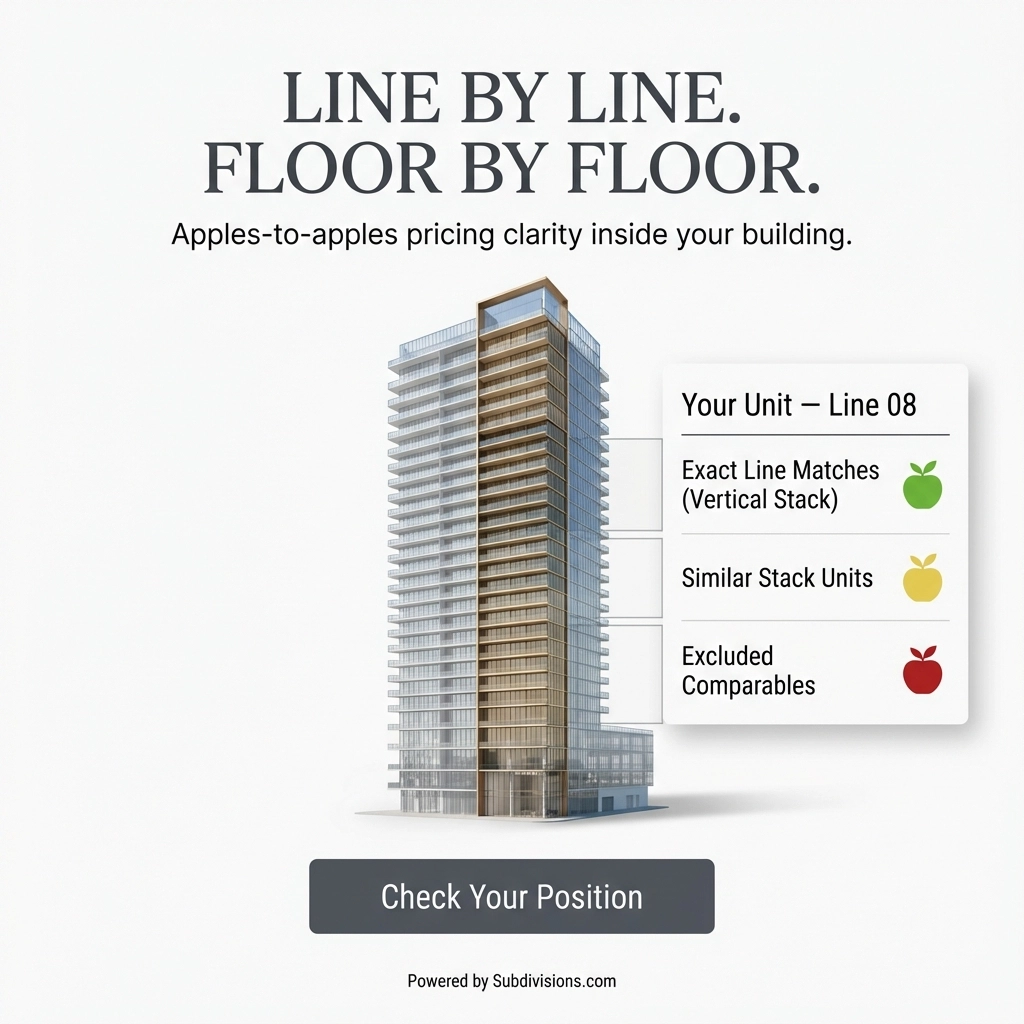

In high-rise buildings, pricing does not distribute evenly across the structure. It moves vertically.

Within a single tower:

• Stack 04 may consistently trade at a premium

• Stack 08 may absorb slower due to exposure

• Upper floors may not scale linearly

• Active competition inside the same line may distort demand

• Identical layouts can show materially different velocity

Two units can share identical square footage and finishes — and still produce materially different outcomes.

Not because the market moved.

Because the stack behaved differently.

Why This Matters at Scale

A 4% positioning variance on a $1.5M condo equals $60,000.

Across 20 units in the same building, that’s $1.2M in exposure.

Across a portfolio of towers, the distortion compounds.

This isn’t dramatic mispricing.

It’s incremental drift.

And incremental drift is the most dangerous type of pricing risk — because it’s easy to miss.

It shows up later as:

• Extended days on market

• Repricing cycles

• Absorption slowdown

• Carry cost expansion

• Capital locked longer than modeled

In institutional settings, small comp misalignment becomes measurable capital friction.

The Problem Isn’t Market Volatility

The problem is comp aggregation.

Traditional tools aggregate horizontally:

By ZIP code

By building

By size bracket

By time window

But high-rise assets compete vertically:

Inside stacks

Across floors

Within exposure groups

Against active competition in the same line

When pricing decisions are based on horizontal aggregation, vertical nuance gets flattened.

That flattening is risk.

The Blind Spot in Conventional BPO & Valuation Workflows

Broker Price Opinions and internal valuation reviews often operate under:

• Time pressure

• Standardized templates

• Building-level comp pulls

• Discretionary floor adjustments

The constraint isn’t expertise.

It’s structure.

Without a system that isolates:

• Line-by-line pricing distribution

• Active vs sold alignment inside the same stack

• Floor-tier clustering

• Stack-specific velocity

Comp selection becomes partially subjective.

Subjectivity at scale becomes variability.

Variability becomes portfolio noise.

Portfolio noise becomes capital risk.

Pricing Risk in High-Rise Assets Is Not Theoretical

It shows up in:

• Underwritten exit assumptions

• Loan-to-value sensitivity

• Re-underwriting events

• Developer release schedules

• Distressed asset disposition

The difference between pricing with vertical stack context and pricing without it is rarely obvious on one unit.

It becomes obvious across 15.

Or 40.

Or 200.

The Infrastructure Gap

The industry has sophisticated macro data.

What it lacks is structured micro-market organization inside buildings.

That is the gap Subdivisions.com addresses.

Not by replacing appraisal methodology.

Not by producing value conclusions.

But by structuring data the way high-rise markets actually behave.

What Structured Micro-Market Intelligence Changes

Instead of pulling comps broadly across a building, structured micro-market intelligence:

• Organizes comparables vertically

• Isolates stack-specific behavior

• Aligns active and sold competition within the same line

• Visualizes pricing distribution inside the building

• Reduces comp selection ambiguity

This reduces incremental pricing drift.

It improves internal defensibility.

It speeds review cycles.

It tightens portfolio consistency.

Where This Matters Most

Subdivisions.com is particularly relevant for:

Institutional Condo Inventory Holders

Pricing alignment across stacks before market exposure.

Developers Managing Remaining Units

Avoiding over-aggregation across vertical lines.

Portfolio Managers

Reducing incremental variance across multiple units in the same tower.

BPO & Valuation Oversight Teams

Standardizing stack-aware comp review.

Asset Disposition Groups

Improving absorption modeling inside dense vertical inventory.

This Is Not an AVM

Automated valuation models attempt to generate a number.

Micro-market intelligence structures the context behind the number.

One predicts.

The other organizes.

One abstracts.

The other isolates.

For high-rise assets, organization reduces risk more effectively than abstraction.

The Capital Impact

In vertical markets, pricing precision is not cosmetic.

It affects:

• Exit timing

• Portfolio IRR

• Carry cost exposure

• Lender confidence

• Capital recycling speed

When pricing is aligned at the stack level, portfolio noise decreases.

When portfolio noise decreases, capital efficiency improves.

That is measurable.

The Shift

Residential real estate is often described as local.

High-rise assets are not just local.

They are structural.

They require vertical intelligence.

Subdivisions.com operates at that structural layer — organizing pricing behavior where it actually competes: inside the building.

Not to replace professionals.

But to reduce the blind spots that quietly cost capital.

In dense vertical markets, pricing risk isn’t horizontal.

It’s vertical.

Comments